Placed in Service (PIS) staff are available to answer questions as you prepare the placed in service application; staff contacts can be found on our main Placed In Service webpage.

Prior to CTCAC issuing IRS Form 8609 and/or FTB form 3521A, the following requirements must be met:

- Projects are required to meet the deadline according to our most current Reg. § 10322(i)(1).

- For projects where conversion to permanent financing has not taken place, projects shall still submit their placed in service package by their deadline. If a project is unable to provide the below listed documents in the initial PIS application because permanent financing has not taken place, those documents shall be submitted within 60 days of the permanent financing conversion date. If a short extension is needed, CTCAC can grant on a case-by-case basis. Please email Diane SooHoo or Marisol Parks for an extension request.

- If below items were not attainable for the initial PIS application submission. These items shall be submitted within 60 days of the permanent financing conversion date:

- Section 2: Item 13

- Section 3: Items 1, 2, 3, and 7.

- Submission of the executed final cost certification (Section 3: Item 1) shall indicate the project's request for issuance of IRS Form(s) 8609 and/or FTB Form(s) 3521A;

- The partnership and CTCAC shall execute the CTCAC regulatory agreement and record the agreement in the official records of the county where the project is located.

- 4% projects - has met and completed California Debt Limit Allocation Committee (CDLAC) RESOLUTION requirements. If there are any discrepancies between the PIS documents and final CDLAC Resolution, the PIS review and Regulatory Agreement drafting will be put on hold until resolved. Contact CDLAC to resolve prior to submitting the PIS package: CDLAC@treasurer.ca.gov

CTCAC shall determine if all conditions of the reservation have been met. Changes subsequent to the initial application, particularly changes to the financing plan and costs or changes to the services amenities, must be explained by the project owner in detail. If all conditions have been met, tax forms will be issued, reflecting an amount of Tax Credits not to exceed the maximum amount permitted by our regulations.

The initial PIS application must be submitted electronically on a USB flash drive by mail. CTCAC will not accept submissions of application documents by email or over the internet. Mail the PIS package to CTCAC, that includes:

- Placed in service package in USB drive format

- Cover letter stating CTCAC Project Number (CA-XX-XXX), Project Name, specify "PIS package"

Attn: Dua Xiong

California Tax Credit Allocation Committee

915 Capitol Mall, Suite 280

Sacramento, CA 95814

PIS Application materials and guidance:

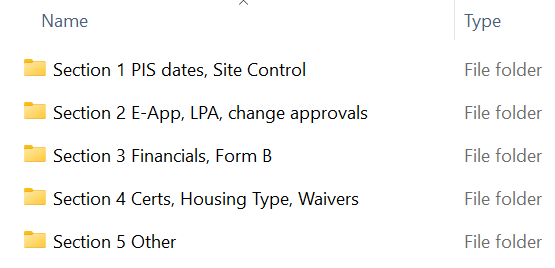

When compiling the flash drive, order the folders according to the sections below. The Electronic Application MUST be an Excel file, be labeled with the project number, and specify “PIS E-App.”

For the attachments, if the same document is applicable under more than one section, please include the document in the first of the sections. To help staff review requirements efficiently, please also include a one-page pdf document in the later sections in place of the document itself, cross-referencing the folder under which the actual document is located. If a section is not applicable to the project, either remove the folder entirely or mark “- NA” in the folder name

Please refer to the following visual as a guide:

Additional steps to help staff review requirements efficiently, please label the attachments according to the name of the document described in the below sections. Abbreviate for longer phrases/names, examples:

- "PIS" for placed in service.

- "HCD" for Housing and Community Development

- "Perm Fin" for Permanent Financing

- "LPA" for Limited Partnership Agreement

- "$3M" for $3,000,000

- "UA" for Utility Allowance

Copies of documents must be legible with reasonably sized font and, when applicable, clear signatures and dates. PDFs should be searchable whenever possible.

SECTION 1: PLACED IN SERVICE DATES AND SITE CONTROL

Guidance:

Documentation of the placed in service date is required. Before submitting the placed in service package, be sure the final placed in service date(s) is accurate and agreed upon by the general and limited partners (developer and investor). Accuracy is important because this date can affect when the credits may be claimed by the limited partner.

For rehabilitation projects, in accordance with Internal Revenue Code (IRC) Section 42(c)(1)(B), the Rehabilitation placed in service date(s) are determined by the owner within the 24-month period of substantial improvement. The owner determined placed in service date(s) shall be entered on the Form B for each building.

For new construction projects, the date of the Temporary Certificate of Occupancy (TCO) or Certificate of Occupancy (CofO) for residential units shall be used as the placed in service date. The placed in services dates on the Form B must match the applicable document (TCO or CofO).

If acquisition Tax Credits are requested, evidence of the placed-in-service date for acquisition purposes is required. The acquisition placed in service date on the Form B must match the grant deed recorded date or final escrow closing statement.

For projects developed under a ground lease, please review CTCAC's Ground Lease Project Requirements

Legal description of the site

- It is important for the CTCAC regulatory agreement to be correctly recorded on title. CTCAC has received and reviewed numerous incorrect or incomplete legal descriptions and continues to expend resources confirming this basic function of ensuring the project owner is providing the correct legal description(s) of a project site. Because legal description errors are easily transmitted from one legal document to another, it is important that project managers and those submitting PIS applications understand how to correctly identify and verify the legal description of a site. While staff understands that legal descriptions may sometimes change, when this occurs it is essential for an explanation to be included in the PIS submission.

- CTCAC has seen an increase in multi-phase projects, scattered site projects, single building multi-project sites, bundled re-syndications, hybrid 9% and 4% credit projects, and other complex physical configurations. While project owners may have a complete understanding of these configurations, the PIS application is often submitted with little or no explanation. Deciphering an accurate representation of these projects from legal description documents can be nearly impossible and typically results in lengthy communications between CTCAC and the project manager. This delays the regulatory agreement preparation, which is the first step in the PIS review.

Required Materials:

PIS Dates:

- New Construction projects: certificates of occupancy for each building in the project. A CofO is required for each building. If the date of the TCO is being used as the placed in service date, then include both the TCO and the CofO.

- Rehabilitation projects: evidence that all rehabilitation is completed;

If Notice of Completion is provided for this requirement, if available, provide the recorded copy. - Acquisition Credits: documentation for applicable acquisition date. Acceptable documentation includes grant deed and/or escrow closing statement for property. For rehabilitation projects developed under a ground lease, a grant deed and/or escrow closing statement should be provided for acquisition of the building(s).

Site Control:

- For projects developed under a Leasehold interest:

- Copy of the executed lease agreement or equivalent DDA;

- If any of these documents have been amended, provide copy(ies) of the amendments;

- Include a copy of the recorded memorandum of lease agreement; if the lease agreement or equivalent DDA was recorded instead of a memorandum, provide the recorded copy(ies);

- If the project is developed under a sublease to a lease agreement, include the sublease and all connecting lease documents to the initial lease agreement;

- For rehabilitation projects, include the recorded grant deed confirming the building(s)/improvement(s) are owned by the partnership (lessee);

- For tribal trust land, the lease agreement between the Tribe and the project owner.

- All other projects, provide one of the following:

- Title report or preliminary title report dated no earlier than 90 days of PIS application submission showing the project owner holds fee title, (title insurance and title commitment not acceptable)

- Recorded grant deed

- For tribal trust land, provide a title status report or an attorney's opinion regarding chain of title and current title status,

Other Required Materials for Regulatory Agreement:

- Legal Description: Provide a Word document or PDF of the project's most current final recorded legal description. This will be the source for the legal description in the CTCAC regulatory agreement and must be up-to-date and accurate. If the legal description provided does not match the submitted site control documents, provide supporting documentation for the legal description.

- Signature Block for Limited Partnership: Provide in a format that allows CTCAC to copy and paste in rich text format.

- Signature Block for Lessor: Provide in a format that allows CTCAC to copy and paste in rich text format.

- Eventual Tenant Ownership: if the project has committed to make Tax Credit Units available for eventual tenant ownership, provide the information described in Reg. § 10325(c)(6):

- evidence of a financially feasible program, incorporating, among other items, an exit strategy, home ownership counseling, funds to be set aside to assist tenants in the purchase of units, and

- a plan for conversion of the facility to home ownership at the end of the initial 15-year compliance period. In such a case, the regulatory agreement will contain provisions for the enforcement of such covenants.

SECTION 2: CTCAC APPLICATION, LIMITED PARTNERSHIP, and CTCAC/CDLAC consent/approvals

Guidance:

An updated Electronic Application (E-App / Attachment 40) is required. Please use the E-App that was last submitted to CTCAC for the preliminary tax credit award/reservation and update it with the PIS information and figures. Do not use a later-version E-App template for the PIS submission. If an updated E-App was submitted to CDLAC after the preliminary reservation and it is a different version, we will not be able to conduct the PIS review using that E-App.

Additional Guidance for updating the E-App: Additional Guidance for PIS E-App Update

For projects where conversion to permanent financing has not taken place:

- If item 13 was not attainable for the initial PIS application submission. This item shall be submitted within 60 days of the permanent financing conversion date.

- Item 1, if any figures have changed after permanent conversion, contact the PIS analyst for the project to obtain the most current agreed upon E-App excel for updating.

Required Materials:

- Updated Electronic Application (E-App / Attachment 40)

APPLICATION WORKSHEET supporting documents:

- Provide a copy of the executed limited partnership agreement (LPA) and any amendments

- Within the LPA, use yellow highlighting to indicate where the LPA complies with the following requirements:

- All projects must comply: All unexpended funds in project reserve accounts shall remain with the project to be used for the benefit of the property and/or its residents:

(See Reserve Requirements Memo and Language on Reserves.pdf) - 9% projects for which all general partners are qualified nonprofit organizations: the partnership agreement must include a Right of First Refusal ("ROFR") for the nonprofit general partner to purchase the project as described in Reg. § 10337(a)(1). This nonprofit requirement is not applicable to awards made before 2016.

- All projects must comply: All unexpended funds in project reserve accounts shall remain with the project to be used for the benefit of the property and/or its residents:

- Within the LPA, use yellow highlighting to indicate where the LPA complies with the following requirements:

- If project elected to change the federal set-aside from 40%/60% to 40%/60% Average Income post-award, election should have been reviewed before PIS submission. If election was approved, include the CTCAC approval email/letter.

- If General Partner(s) have changed since Preliminary Reservation, include the CTCAC approval letter/email.

- Not applicable to projects where request for assignment is not necessary per CTCAC Memo: Consent Agreements Memo.pdf

- If Management Company(ies) have changed since Preliminary Reservation, then provide CTCAC approval letter/email.

- If training was required as conditioned in the Preliminary Staff report, then provide evidence the following training was completed:

- CTCAC ownership/management training course

- Project operations

- On-site certification training

- Fair housing law

- Manager certification in IRS Section 42 program requirements from a CTCAC-approved, nationally recognized entity

- Provide utility allowance (U.A.) schedule, amounts should match the U.A. amounts in the CTCAC application:

- Utility allowance estimate as required by 26 CFR Section 1.42-10(c) and Reg. § 10322(h)(21).

- Projects utilizing California Utility Allowance Calculator (CUAC), provide approval letter issued by CTCAC compliance.

- Use of CUAC requires a quality control review and CTCAC approval at the PIS stage, requirements are currently outlined on CTCAC's CUAC webpage: California Utility Allowance Calculator

- HOME projects utilizing alternative equivalent U.A. model allowed by HUD Regulations instead of Public Housing Authority (PHA) U.A. schedule, provide approval/acknowledgement letter issued by CTCAC compliance.

- Use of any of the U.A. models below requires CTCAC compliance review and approval/acknowledgement, please contact Compliance Manager - Ted Johnson, Ted.Johnson@treasurer.ca.gov if a review is needed:

- CUAC

- HUSM- HUD Utility Schedule Model

- Project specific methodology such as the HUD Multifamily Housing Utility Analysis

- Utility Company Estimate (PG&E)

- Use of any of the U.A. models below requires CTCAC compliance review and approval/acknowledgement, please contact Compliance Manager - Ted Johnson, Ted.Johnson@treasurer.ca.gov if a review is needed:

- When U.A. schedule not required:

- If project owner is paying for all U.A.s.

- Master-Metered Utilities, Public Housing Authority (PHA) pays for consumption.

- For projects charging water, trash, and/or sewer utility allowance, units must be individually metered. If applicable, ensure Owner Certification provides certification units are individually metered.

- Rent limits: Provide documentation of CTCAC published Income and Rent Limits the project is utilizing to charge actual rents.

- Unit mix and targeting: If the unit mix or income targeting has changed, provide the CTCAC approval letter/email:

- 9% projects: any change in unit mix or income targeting after initial award of tax credit must be approved by CTCAC.

- 4% projects: any change in unit mix or income targeting after preliminary reservation, except for changes that result in deeper income targeting, must be approved by CTCAC.

- Gross Rent Floor election: If actual rents are greater than rent limit year because project elected to fix gross rent floor, include documentation of the gross rent floor election.

- Resyndication Projects - If rent limits are hold harmless rent limits, then provide table rent limits being used that was established under the previous allocation.

- Minimum Operating Expenses: If project is utilizing operating expenses up to 15% less than required for underwriting, pursuant to Reg. § 10327(g)(1), then provide documentation from the final equity investor and permanent lender they have agreed to such lesser operating expenses.

- Threshold Basis limit Adjustments: Provide required CTCAC documentation per Reg. § 10327(c)(5) for all requested basis adjustments. Any applicable dollar amounts hard entered into the table must correspond to the cost certification and Sources and Uses Budget.

- Prevailing Wages, 20% increase - Provide documentation that confirms there was oversight of prevailing wages payment by the public entity or a document that confirms oversight was performed by a third party.

Note: Do not provide the wage determination documents or an owner certification that confirms the general requirement. - Prevailing Wages, 5% increase - Prevailing wage requirement subject to (A) or (B) below:

A project labor agreement within the meaning of Section 2500(b)(1) of the Public Contract Code that requires the employment of construction workers who are paid at least state or federal prevailing wages.

(A) Provide a copy of the project labor agreement, if not provided in the original application.

Use of a skilled and trained workforce, as defined in Section 25536.7 of the Health and Safety Code, to perform all onsite work within an apprentice able occupation in the building and construction trades.

(B) Provide a copy of the enforceable agreement with the public entity or other awarding body; notate or highlight any sections that document the skilled and trained workforce requirement. - For remaining threshold basis limit adjustment items that need certification by 3rd party architect or energy analyst, ensure items are certified in the architect certification or energy analyst certification. Certification templates are located on our main Placed In Service webpage.

- Prevailing Wages, 20% increase - Provide documentation that confirms there was oversight of prevailing wages payment by the public entity or a document that confirms oversight was performed by a third party.

CTCAC Competitive Projects: "High Cost" Test - Any project may be subject to negative points if the project's total eligible basis at placed in service exceeds the revised total adjusted threshold basis limits for the year the project is placed in service (or the original total eligible threshold basis limit if higher) by the following percentages:

- 30% for projects awarded before 2016

- 40% for projects awarded 2016 and later

If it is necessary for the E-App to demonstrate compliance, projects may request staff to have the Threshold Basis Limit figures updated for the year the project is placed in service before submitting the PIS application. Provide the PIS date documentation listed in Section 1 to evidence PIS year.

- Other Required Materials for Application worksheet:

- CTCAC and/or CDLAC approval email for any changes to the Application worksheet.

- If any sections are inconsistent with the final CDLAC Resolution and an update is not required, provide email/correspondence from CDLAC confirming a revised Resolution is not necessary.

- If the number of buildings has changed since preliminary reservation, provide documentation and or explanation for this change.

FINAL TIE BREAKER worksheet, supporting documents:

- Provide an update to the breakdown of the off-site costs originally provided in the application's Tab 12 construction and design description (Attachments - Exhibit A: Const. & Design tab).

SECTION 3: FINANCIALS and FORM B

Guidance:

For projects where conversion to permanent financing has not taken place:

- If items 1, 2, 3, 7 were not attainable for the initial PIS application submission. These items shall be submitted within 60 days of the permanent financing conversion date.

- Item 13, if any tax credit and/or eligible basis figures have changed after permanent conversion, contact the PIS analyst for the project to obtain the most current agreed upon Form B excel for updating.

Changes made to a project's financing structure or type of financing

- CTCAC staff must verify the permanent financing sources and amounts. This is part of CTCAC's responsibility to ensure that a project is not over subsidized and that CTCAC allocates no more credit than necessary.

- It is the owner's responsibility to include an explanation of changes to a project's financing structure or types of financing and ensure these changes meet program requirements. The credit reservation and application underwriting were based on the financing structure presented in the original application. Significant and/or unexplained changes will delay a PIS application and it is not uncommon for changes to be out of compliance with CTCAC regulations. Commonly occurring examples include:

- Missing documentation for a financing sources;

- Inadequate documentation of the final loan amount for a construction-to-perm conversion;

- Changes made to resyndication Transfer Event commitment requirements;

- Changes in required developer fee contributions;

- Changing from a donation to a soft loan;

- Unapproved reductions of public funding sources that provided tiebreaker advantage to competitive applications.

Acquisition Costs and Underwriting

- The land cost and the value of existing improvements in the Sources and Uses Budget must meet the underwriting requirements outlined in CTCAC Reg. § 10327(c)(6). It is the owner's responsibility to ensure compliance with these acquisition cost underwriting requirements.

- If any changes to the site control in the original application are contemplated, these must be authorized by CTCAC in advance since the credit reservation was approved pursuant to the application's site control and underwriting. An alternate or subsequent appraisal cannot be used to increase the land cost, existing improvements, or eligible basis values presented in the original application.

Resyndication Requirements:

- Use Checklist and Q&A: Transfer Event Questionnaire to determine if project has met all requirements.

- Review the CTCAC staff report for any resyndication and transfer-event terms, requirements, and conditions as you prepare the PIS application.

Requesting Issuance of tax forms: Submission of the executed final cost certification (item #1) shall indicate the project's request for issuance of IRS Form(s) 8609 and/or FTB Form(s) 3521A.

Required Materials:

Sources and Uses WORKSHEET, supporting documents:

- Cost and Eligible Basis Certification:

an audited certification, prepared and signed by an independent Certified Public Accountant identified by name, under generally accepted auditing standards, with all disclosures and notes. The Certified Public Accountant (CPA) or accounting firm shall not have acted a manner that would impair independence as established by the American Institute of Certified Public Accountants (AICPA) Code of Professional Conduct Section 101 and the Securities and Exchange Commission (SEC) regulations 17 CFR Parts 210 and 240. Examples of such impairing services, when performed for the final cost certification client, include bookkeeping or other services relating to the accounting records, financial information systems design and implementation, appraisal or evaluation services, actuarial services, internal audit outsourcing services, management functions or human resources, investment advisor, banking services, legal services, or expert services unrelated to the audit. Both the referenced SEC and AICPA rules shall apply to all public and private CPA firms providing the final audited cost certification. In order to perform audits of final cost certifications, the auditor must have a peer review of its accounting and auditing practice once every three years consistent with the AICPA Peer Review Program as required by the California Board of Accountancy for California licensed public accounting firms (including proprietors); and make the peer review report publicly available and submit a copy to CTCAC along with the final cost certification. If a peer review reflects systems deficiencies, CTCAC may require another CPA provide the final cost certification. This certification shall:- include an unqualified audit report, as identified by the certified public accountant, reflect all costs, in conformance with 26 CFR § 1.42-17. Projects developed with general contractors who are Related Parties to the developer must be audited to the subcontractor level. The Cost Certification Statement template is located on our main Placed In Service webpage;

- include a CTCAC provided Sources and Uses form reflecting actual total costs incurred up to the funding of the permanent source(s). The Sources and Uses Budget worksheet template in the E-App may be use;

- certify that the CPA has not performed any services, as defined by AICPA and SEC rules, that would impair independence; and

- include the auditor's most recent peer review

- Certified Public Accountant (CPA) certification of all expenditures for the project up to the funding of the permanent source(s), and shall include permanent financing conversion date. For any sources the CPA is unable to certify, the PIS package must include supporting documentation, such as loan agreements, deeds of trust, promissory notes, or other relevant instruments.

- Deferred developer fee notes and/or agreements must be included, and the interest rates of such notes shall not exceed eight percent (8%).

- For tax-exempt bond (4%) projects that received Tax Credits under the provisions of Reg. § 10326, provide a certification from a third-party tax professional stating the percentage of aggregate basis (including land) financed by tax exempt bonds. The percentage of tax-exempt bond financing must exceed 50% of the aggregate basis (including land).

- If line items in Sources and Uses Budget (cost and basis) do not match exactly with the Final Cost Certification, then provide an explanation and indicate which line items to reference for staff to reconcile discrepancies.

- Acquisition costs:

- New Construction projects: Once established in the initial application, the acquisition cost of a new construction site shall not increase except for increases permitted under Reg. § 10327(c)(6). If increase is allowed, provide CTCAC approval letter/email correspondence.

- Projects with Existing Improvements: Neither the purchase price nor the basis associated with existing improvements, if any, shall increase except as permitted under Reg. § 10322(h)(9)(A) or by a waiver pursuant to Reg. § 10327(c)(6) for projects basing cost on assumed debt. If increase is allowed, provide documented evidence of the sum of third-party debt encumbering the property that will be assumed or paid off.

- Operating reserve requirement - If a Demand Note or Letter of Credit, of an equal amount, is provided in lieu of a three-month capitalized operating reserve, provide the executed Demand Note and/or Letter of Credit. If the Payee/Lender/Holder of the Demand Note and/or Letter of Credit is a related party to the project owner, include an audited certification from a third party certified public accountant that the project owner has sufficient funds to successfully accomplish the financing.

- Resyndication projects:

- If applicable, provide Resyndication Certification that demonstrates the project qualifies for a partial/full waiver of Transfer Event Short Term Work requirements:

Transfer Event- If the sources listed in the resyndication certification for the transfer event do not match the sources shown in the Sources and Uses Budget worksheet of the E-App, submit documentation that explains the discrepancies. This information should allow staff to reconcile the differences.

- If the project does not qualify for waiver of Transfer Event Short Term Work requirements, the amount of short-term work should be excluded from eligible basis.

- For resyndication requirements and conditions stated in the Staff Report, ensure all requirements are fully documented within the PIS application. As applicable, provide documentation demonstrating that the requirements have been satisfied.

- If applicable, provide Resyndication Certification that demonstrates the project qualifies for a partial/full waiver of Transfer Event Short Term Work requirements:

- Commercial costs in budget - If the commercial space is not owned by the Limited Partnership (note: ownership by related parties to the Limited Partnership does not constitute ownership by the Limited Partnership), provide documentation of separate, non-tax credit funding sources dedicated specifically to the construction of the commercial space. Examples:

- Documentation for sale of commercial space must include dollar figure sale proceeds

- If the hard lender specifies a portion of the loan is underwritten using commercial income, the project must provide loan documentation demonstrating the commercial underwriting assumptions.

Basis and Credits WORKSHEET, supporting documents

- Investor Certification: provide a certification from the investor or syndicator of equity raised and syndication costs in a Committee-provided format: See Template on the CTCAC website

Letter must include the following information:

- Total funds raised from the sale of the tax credits (gross equity),

- Total tax credits (federal and state),

- An itemization of all syndication costs,

- Net payment to the partnership,

- The tax credit factor(s),

- Type of sale (public syndication/private offering/private Regulation offering)

- The pay-in schedule

- Include letterhead or specify investor name below signature.

Note: A letter from a financial consultant will not be accepted.

- Certification should include an equity amount and a tax credit price based on 100% of the tax credits (not solely the limited partner's/investor's portion). The Excel application must calculate 100% of the tax credits, not the 99.99% limited partner/investor portion.

- If the investor certification calculates 99.99% of the equity and credits, then the Excel application must include the general partner equity in the Tax Credit Equity total, and the tax credit factor for the application Basis and Credits must be adjusted accordingly. Please contact CTCAC staff with questions.

- If the project includes solar equity and/or historic tax credit equity, and those proceeds are being provided by the same investor purchasing the Low-Income Housing Tax Credits (LIHTC), the investor letter must clearly itemize the separate equity funding sources. Please refer to the CTCAC template for the required format.

- STATE TAX CREDITS

- Link here: Request Issuance, including Certificated State Credits

- Provide documents for requesting state tax credit issuance

- If project elects to certificate their state tax credits, provide additional documentation as required.

- FEDERAL APPLICABLE RATE(s)

- Tax-Exempt Bond projects, if applicable, provide CTCAC approved Election to Fix Credit Percentage at Bond Issuance

- 9% Projects, if applicable, provide CTCAC approved Exhibit B to the Carryover Allocation- Election to Fix Acquisition Credit Percentage

- Projects requesting Acquisition Credits that elected to Fix Credit Percentage at Bond Issuance, if the credit percentage was fixed at bond issuance but the acquisition date occurred earlier than the month and year of the bond issuance date, as evidenced by the grant deed or final escrow closing statement, the acquisition applicable rate is based on the earlier date of the acquisition, not the bond issuance date.

(Not applicable to projects required to use 4% minimum rate per IRS)

FORM B

- Form B – Eligible Basis by Building

An itemized breakdown of placed-in-service dates, unit mix, eligible basis, etc. shown separately for each building;- Include a copy of the signed PDF version along with the matching Excel file. The completed and fully executed CTCAC Form B must be signed by both the Owner and the Investor. The Excel version is required for staff to prepare the Regulatory Agreement and the 8609 forms.

- For projects that have not yet converted to permanent financing, the Part 3: Eligible Basis column may be left blank. At this stage, only the project owner's signature is required on Form B.

- Read the Form B "Instructions to Complete" worksheet. Additional guidance and instructions are provided within this worksheet on how to complete the Form B accurately.

- If project has buildings located in both QCT/DDA locations and Non-QCT/DDA locations, then provide two Form B Excels:

- Buildings located in both QCT/DDA locations

- Buildings not located in QCT/DDA locations

- 4% projects only - If updating QCT/DDA status for 130% increase for new construction/rehabilitation eligible basis, then provide HUD Map for the year the project is qualified. If the bond issuance date and placed in service date are not both in the same year as the applicable DDA/QCT HUD Map, at least one of the necessary actions (bonds issued and buildings placed in service) must occur in the same year as the applicable DDA/QCT HUD Map and the other necessary action must occur in a year subsequent to the year of the applicable DDA/QCT HUD Map.

Other Form B supporting documents:

Manager's unit: https://website-qa.treasurer.ca.gov/sites/default/files/2026-03/manager-unit-memo.pdf- If the manager's unit is also a restricted low-income unit, then that unit is no longer exempt. Provide an employment agreement, lease agreement, and/or employment contract for CTCAC to verify that the employment of on-site manager, assistant manager, and/or maintenance personnel is not tied to the lease and/or residence.

- If the manager unit is a single-family house/dwelling, indicate in the Owner Certification (Section 4, Item 1 of this webpage) whether the owner elects for CTCAC to assign an IRS Building Identification Number (BIN) (CA-XX-XXXXX), or elects not to have a BIN assigned.

Carryover Agreement:

- If the Project had a Credit Exchange (High Rise/Disaster/etc.), provide the updated Carryover Agreement with new BINs

- Provide documentation from the IRS assigning the federal Taxpayer Identification Number (TIN) for the Limited Partnership (project owner).

SUBSIDY CONTRACT CALCULATION WORKSHEET supporting documents:

- Include the most current rental subsidy contract with the monthly contract rent for each bedroom/unit type.

- Supplemental documents if applicable: If monthly contract rents for each bedroom/unit type are not stated in the contract, provide supplemental documentation from entity that issues the rental subsidy for this information.

SECTION 4 CERTIFICATIONS, Housing Type requirements and Waiver approvals

Guidance:

Competitive application changes: Competitive applications committed to various point category requirements and scoring criteria. Any changes to these commitments must be approved by CTCAC/CDLAC; applicants and owners should contact CTCAC/CDLAC staff in advance of making such changes. Examples of these changes include but are not limited to:

- Unit mix

- Income targeting

- Bedroom type

- Manager unit increases or decreases

- Service amenities

- Property management

- Final tie breaker score

- Public financing

- Etc.

Items 1, 8, 9, 10, 11, and 12 below (certification documents) are located on our Placed In Service webpage.

Required Materials:

Owner Certifications:

- Provide a completed owner certification and any related documentation, including post-reservation project change approvals and waiver approvals.

- If different services were approved post-award, then provide evidence of CTCAC approval and all related documents (MOUs, service provider contract, etc.).

- For multiphase projects or other projects with shared use of common areas, community space, facilities, services, or staffing, provide a description of the shared items and include the Joint Use Agreement between the owners.

- Legal Opinion(s), if applicable

- If the project includes a legal separation or subdivision of a building that is not a condominium plan: provide a legal opinion of how the legal separation meets the IRS definition of a building. The opinion must include a summary of the common area and building access ownership structure and any shared use agreements.

- Colored photographs of the completed building(s):

- Building Exterior - Signage location, pictures of each building

- Unit interiors - Sample pictures of each type of unit

- Facilities/amenities (community building/areas, recreational areas, etc.)

- For projects awarded housing type points, provide these additional colored photos:

- LARGE FAMILY: Include photos of:

- Unit dishwasher

- Laundry facility

- Outdoor play/recreational facilities (ages 2-12)

- Outdoor play/recreational facilities (ages 13-17)

- SENIOR: Include photos of:

- Elevator (projects over 2 stories)

- Laundry facility

- Accessible unit interiors

- SRO (Single Room Occupancy): Include photos of:

- Laundry facility

- One bath for every 8 units

- Kitchen area/facility if not provided in every unit

- SPECIAL NEEDS: Include photos of:

- Laundry facility

- Accessible unit interiors

- Special Needs, SRO combined (Projects awarded under Dec 2017-April 2020 CTCAC Regulations)

- Laundry facility

- Accessible unit interiors

- One bath for every 8 units (if project has SRO units)

- Kitchen area/facility if not provided in every unit (if project has SRO units)

- LARGE FAMILY: Include photos of:

- NONPROFIT HOMELESS ASSISTANCE SET-ASIDE AWARDS (beginning in 2017):

- Provide documentation of homeless assistance referral system: coordinated entry/access system, county health department list of frequent health care users, or behavioral health department list of persons with chronic behavioral health conditions who require supportive housing; and

- Provide the MOU with the relevant department or system administrator. See Reg. § 10315(b).

- MINIMUM CONSTRUCTION STANDARDS 10325(f)(7)(B)-(I):

- Either the project architect or the energy analyst shall provide this certification.

- Certification not required if project meets a program listed in Reg. § 10325(f)(7)(M)(ii) provide evidence if applicable.

- Waivers for Rehabilitation project: Include any waivers that were approved in advance by the Executive Director for the requirements of subdivisions (f)(7)(B) through (I).

- Accessibility Certification:

- Certification from the project architect or CASp

- Include any waivers that were approved in advance by the Executive Director for accessibility requirements of 10325(f)(7)(K)

- 10325(c)(8)(B): Enhanced Accessibility and Visitability, provide certification if applicable

- Energy Analyst Certification:

- 10325(f)(7)(A): Requirement for Rehab projects, 10% Min Con Standard – must be certified in Energy Analyst Certification unless meets exception by meeting a program listed in 10325(f)(7)(M)(i). Provide evidence for exception if applicable.

- Include any waivers that were approved in advance by the Executive Director for the requirements of subdivisions (f)(7)(A).

- 10327(c)(5)(B): Threshold Basis Limit adjustments for energy efficiency/resource conservation/indoor air quality items, provide certifications to any applicable items listed in the certification. (Reference: PIS E-App: Threshold Basis Limit Table - Item E Features)

- 10325(f)(7)(A): Requirement for Rehab projects, 10% Min Con Standard – must be certified in Energy Analyst Certification unless meets exception by meeting a program listed in 10325(f)(7)(M)(i). Provide evidence for exception if applicable.

- Architect Certification

- Required for all projects: Fair Housing requirements

- 10327(c)(5): Threshold Basis Limit adjustments, provide certifications to any applicable items listed in the certification.

- All applicable CTCAC and CDLAC items project committed to must be certified in Architect Certification.

- Seismic upgrading of existing structures, and/or projects requiring on-site toxic or other environmental mitigation: provide documentation from the project architect or seismic engineer certifying to the costs associated with such work.

- Sustainable Building Methods Points

- Sustainable Building Methods Points Certification:

- 10325(c)(5) requirements, certification(s) required for items where CTCAC points were awarded.

- Tax Exempt Bond projects: certification(s) required for any applicable items in the CDLAC Resolution.

- Sustainable Building Methods Points for green program: Projects receiving points from CTCAC or CDLAC for meeting a recognized green building program per CTCAC Regulations (e.g., LEED, GreenPoint Rated Multifamily, Passive House, etc.) must submit a copy of the certificate issued by the applicable program

- Sustainable Building Methods Points Certification:

- Rehabilitation projects awarded tax credits prior to 2016, with gas-fired appliances must provide the results of Combustion Appliance Safety (CAS) testing by a qualified energy analyst unless all gas-fired appliances were replaced as part of the rehabilitation work. All units must be tested and all "test out" results must be "Pass."

The Executive Director may waive any of the above submission requirements if not applicable to the project.