Vol. 1, No. 5, Published September 9, 2015

Summary of Ratings and Borrowing Costs

Where Does California Fit In?

Event after recent improvements, California�s bond ratings still remain lower than all but two rated states: Illinois and New Jersey. (See a detailed comparison.)

However, for California, holding the higher rating levels over time is what matters most. Lower ratings provoke investors to demand higher yields, which translates into higher borrowing costs.

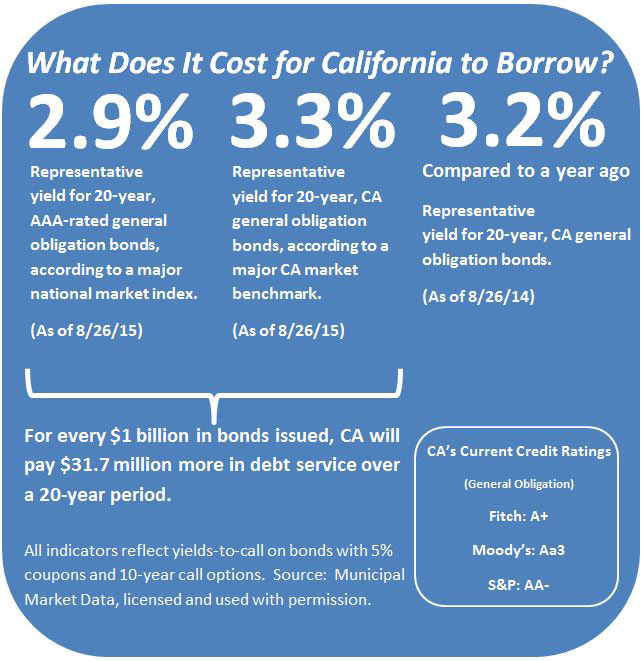

The State�s recent 20-year yield sat at 3.26 percent, higher than the 2.88 percent yield on a national benchmark of AAA-rated bonds, a difference of 0.38 percent. (See Figure 5.)

Compared to the prior month, the nominal yield on the California benchmark rose by 0.07 percent, while the nominal yield on the national benchmark dipped by 0.06 percent.

The difference between the two benchmarks one year earlier was slightly narrower: California�s yield was 3.17 percent, while that same national benchmark was at 2.86 percent, a difference of 0.31 percent.

How should the diverging benchmarks be explained? California engages in two basic borrowing cycles each year, the first in late winter and the second in later summer and early fall. This pattern is dictated by the budget cycle, which requires that the Governor propose a budget each January and update it in early summer for the Legislature�s deliberation and adoption. During the period of time when policy-level decisions may change the dynamics of the budget, the State refrains from entering the market in order to assure investors that the financial information being provided is as current as possible. As a result, when the State does enter the market, there are occasions when California dominates the market to a degree that the benchmarks diverge because of the simple law of supply and demand. When there are abundant California bonds available, the benchmarks tend to temporarily widen.

Figure 5: Borrowing Costs

What does this mean for California taxpayers?

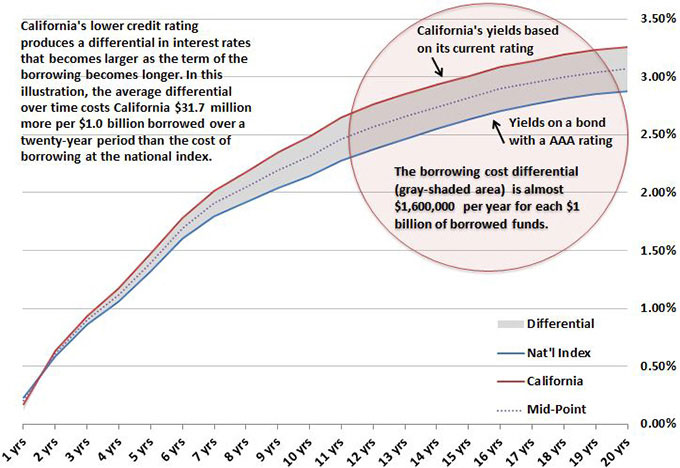

In general, for every $1.0 billion in bonds issued, the State will incur higher borrowing costs as a result of investors demanding investment yields. The result in such a scenario would be about $31.7 million in higher debt service over a 20-year period compared to the national benchmark of AAA-rated, tax-exempt bonds. (See Figure 6.). This compares to lower debt service of $20.5 million illustrated in last month's edition.

After dipping last month from $24 million to $20.5 million over a 20-year period for each $1.0 billion borrowed, this measure has expanded. This is probably a result of a supply-demand imbalance that results from the timing of the sale.

Figure 6: Comparing California's Borrowing Costs to a National Benchmark

Source: Municipal Market Data as of 8/26/15

When it comes to understanding why investment yields and borrowing costs behave this way, it helps to look at long-term trends.

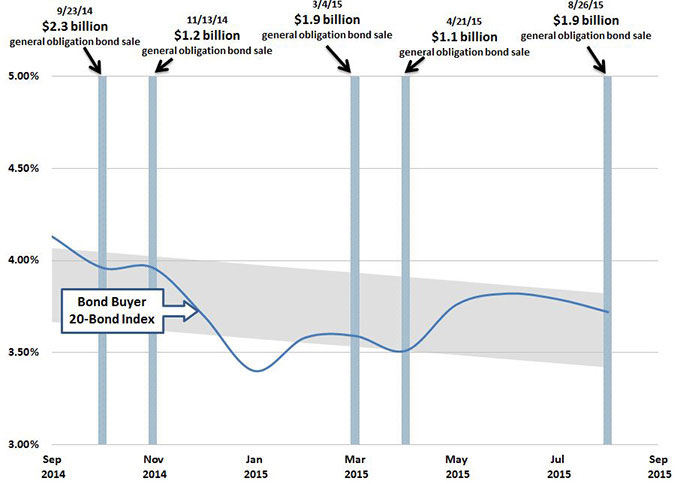

Figure 7, below, shows the one-year trend in another widely used index, the Bond Buyer 20-Bond Index, over the past year. California�s most recent offerings are shown as vertical bars.

The grey band in Figure 7 represents the normal variance around a long-term trend, which can be thought of as the center of the grey band. The blue line represents the changes in the trend over time. In the spring, California enjoyed a market environment where the blue line showed a strong tendency to reside in the lower part of the grey band, which represented an opportunity to borrow money less expensively. But like all financial markets, circumstances change and by late summer, the trend line was residing in the top part of the variance boundaries. The result was marginally higher borrowing costs. This is a normal occurrence. It is not appropriate in public finance to engage in �market timing� because very few folks are able to predict short-term movements in interest rates with a high degree of precision. Accordingly, the objective is to stay within the grey band.

Figure 7: One-Year Trend of Interest Rates, Selected California Borrowings Shown as Vertical Bars

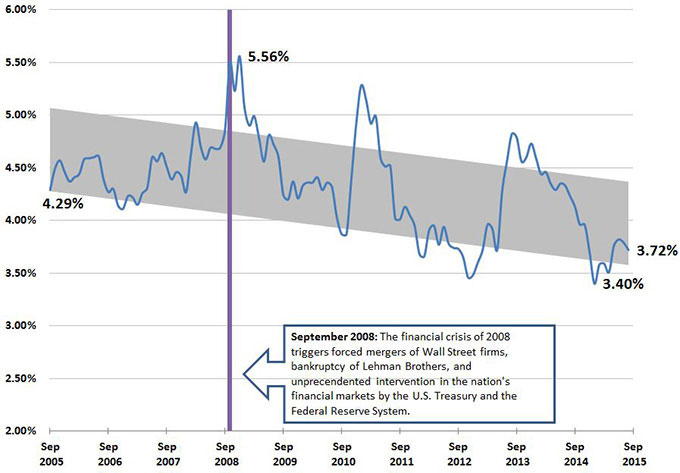

Interest rates on State and local government bonds are lower than they were a decade ago. Figure 8 also uses the Bond Buyer 20-Bond Index, but over a longer 10-year period.

Despite the fluctuation of rates over this longer period, it�s important to remember that this index is still more than one-half percent lower than it was 10 years ago. Borrowing at today�s rates is, by comparison, a bargain versus borrowing 10 years ago.

After breaking out below the long-term trend earlier this year, this widely followed index is now moving back toward the trend line. This means that much of the recent movement is a reversion to that trend line rather than an unexplained spike in rates.

Figure 8: 10-Year Trend of Interest Rates on State and Local Government Bonds